North Carolina’s remarkable economic renaissance over the past decade has been a model of fiscal responsibility and tax reform. The state’s General Assembly has progressively eliminated inefficiencies and lowered barriers to growth, catapulting the Tar Heel State into national prominence as a premier business destination. However, one glaring obstacle persists: the franchise tax, a relic of a bygone era that hinders investment, penalizes entrepreneurship, and generates minimal revenue.

State lawmakers should repeal the franchise tax in 2025, continuing the state’s trajectory toward economic leadership.

A job-killing, growth-deterring tax

The franchise tax is not a tax on fast-food restaurants. It is a yearly tax on any business’s net worth, based on its assets minus liabilities, with additional adjustments. Companies must pay it even if they don’t turn a profit, making it especially tough on startups and struggling businesses. It applies to any company doing business in North Carolina, even if they don’t have a physical location.

It is an inherently flawed approach that punishes capital investment and business growth. Unlike corporate income taxes, which fluctuate based on profitability, the franchise tax is due annually — even when businesses operate at a loss. This dynamic discourages investment in new facilities, equipment, and jobs, particularly during economic downturns.

Small businesses bear a disproportionate burden. Independent contractors and sole proprietors organized as LLCs often face the $200 minimum franchise tax, even if they generate no income or hold no assets. This is a direct disincentive for entrepreneurial ventures that would otherwise contribute to the state’s economic vitality.

High complexity, low returns

The franchise tax is notorious for its complexity. A May 2024 report by the John Locke Foundation’s senior vice president for research, Brian Balfour, notes that its calculation involves apportioning net worth across multiple states and adjusting for affiliated indebtedness. These complications increase business compliance costs and create opportunities for costly audits and fines.

For all its harm, the tax generated a mere 2.2% of General Fund revenue in Fiscal Year 2023-24, about $742.3 million of the state’s $33.7 billion collected, money businesses could not reinvest or disperse as wages. This share will decline further as liabilities are capped in the coming years. Thus, the franchise tax creates an outsized burden for negligible fiscal gain.

The national trend: eliminating franchise taxes

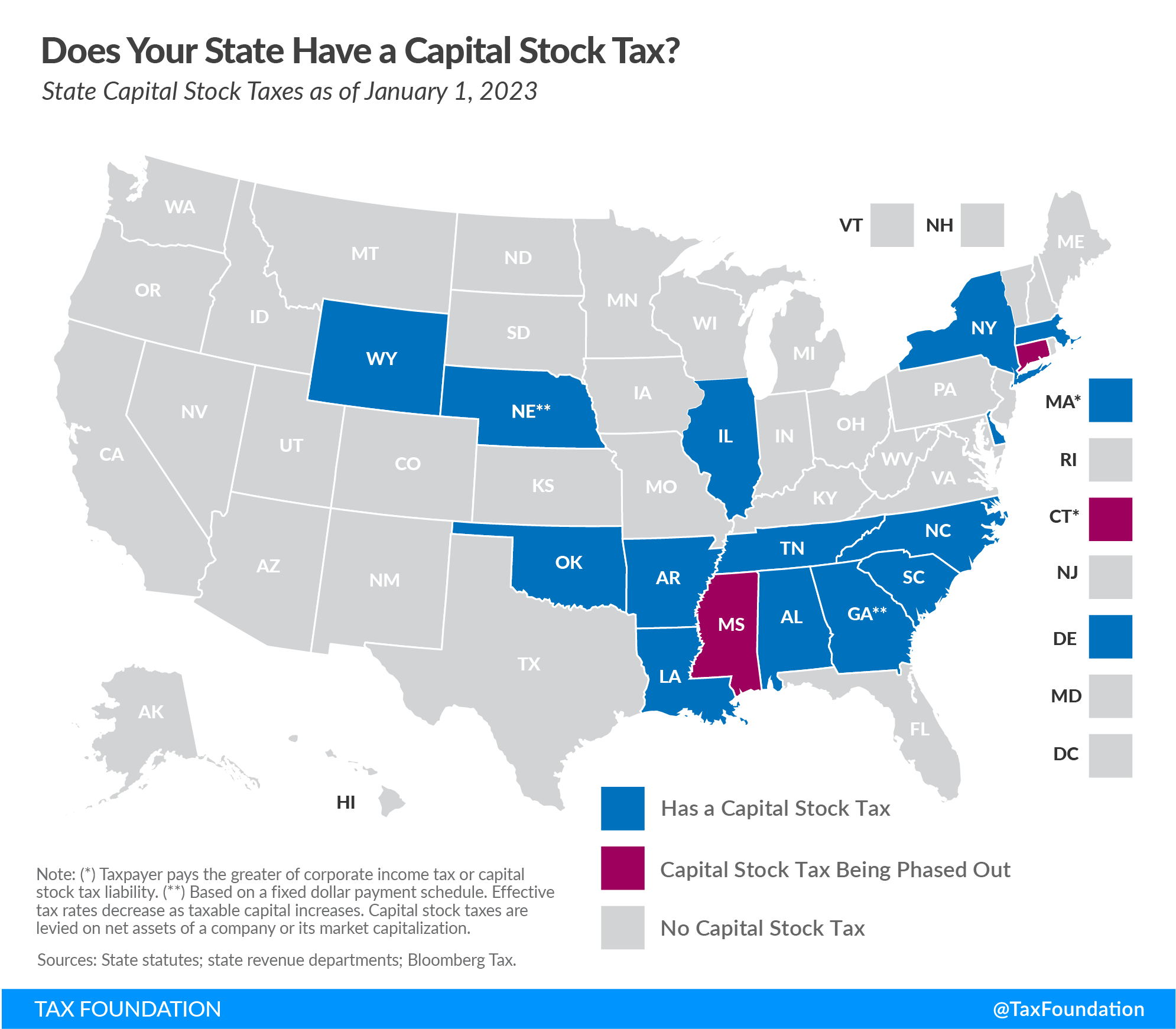

North Carolina is one of only 15 states that still impose a franchise tax. Other states are rapidly abandoning this counterproductive policy. Connecticut, Mississippi, and Oklahoma have taken steps to repeal or phase out their franchise taxes, citing the same economic inefficiencies North Carolina faces. As these states reap the benefits of greater investment and job creation, North Carolina risks being left behind.

The franchise tax is a disincentive for companies to make physical investments in North Carolina because it directly penalizes businesses for growing their capital base. By taxing a company’s net worth — rather than its income — the tax discourages the purchase of equipment, construction of facilities, and other capital-intensive investments that drive economic growth and job creation. Unlike corporate incentive programs, which selectively target certain businesses and projects, repealing the franchise tax would create a broad-based, equitable improvement to the state’s business climate. This approach eliminates distortions caused by incentives and fosters organic, market-driven investment across all sectors.

The state Department of Commerce spends a good deal of time and energy on corporate incentive programs like the One North Carolina Fund and the Job Development Investment Grant (JDIG). These programs aim to attract business investment by offering lucrative incentives. Still, this effort is fundamentally undermined by the state’s franchise tax, which penalizes companies for accumulating capital and investing in growth. Offering incentives to lure businesses while simultaneously taxing their net worth creates a contradictory policy environment that discourages the very investments One North Carolina and JDIG are designed to encourage. Instead of relying on selective incentives, North Carolina should focus on eliminating barriers like the franchise tax, fostering a more predictable and universally competitive business climate.

The franchise tax is fundamentally unjust. It penalizes businesses for accumulating capital, a vital driver of future growth. As the John Locke Foundation report highlights, this type of tax reduces the resources available for job creation, wage increases, and innovation. Moreover, it is not a one-time privilege tax but levied annually.

A logical next step

This tax is a roadblock to economic progress, stifling entrepreneurship while offering minimal returns to state revenue. Eliminating it is more than prudent fiscal policy — it declares North Carolina’s commitment to fostering opportunity and prosperity.

By repealing the franchise tax in 2025, state lawmakers can cement the legacy of the transformative tax reform of the past 12 years, unleashing investment, fueling job creation, and securing North Carolina’s reputation as the nation’s premier business destination.

{kind=link}